Global PC Shipments Exceed Forecast; Apple Moves to #5 Spot, According to IDC

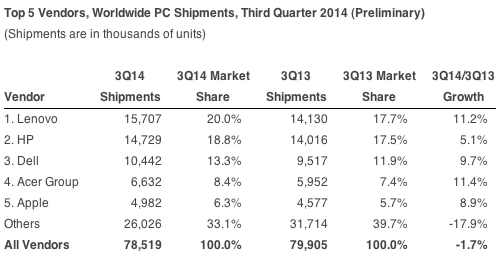

Worldwide PC shipments totaled 78.5 million units in the third quarter of 2014 (3Q14), a year-on-year decline of -1.7% and a sizable improvement over the forecast of -4.1%, according to the International Data Corporation (IDC) Worldwide Quarterly PC Tracker.

Many of the trends from the second quarter remained relevant and contributed to the 3Q14 results. Commercial PC purchases played a key role in many markets, with the top three vendors — Lenovo, HP, and Dell — all showing solid year-on-year growth. Conversely, fierce competition and a spiral toward tablet-like prices helped to further consolidate the market. Shipments of entry systems, including Chromebooks, continued to inject an important source of volume and sustained improved consumer demand in certain markets over recent quarters.

On a geographic basis, mature markets still drove the market, with North America and parts of Europe seeing significant improvements across segments. Although Windows XP migrations has slowed, an improved business outlook, tablet saturation in some markets, and expanded offerings of competitive notebooks have factored in recent positive trends.

Emerging regions as a whole proved disappointing, although stronger than expected consumer demand in Asia/Pacific, spurred by the continued expansion of entry-level portable PCs and helping to redirect consumer attention back toward PCs, provided a silver lining.

“Although shipments did not decline as much as feared, these preliminary results still show that 3Q14 was one of the weaker calendar third quarters on record in terms of sequential growth. The third quarter has historically been driven by back-to-school sales and renewed business purchasing, which were weaker than normal this year,” says Jay Chou, Senior Research Analyst, Worldwide PC Trackers. “The current growth of lower-priced systems, while encouraging in the short run, brings concern for the long term viability of vendors to adequately remain in the PC space.”

“PC shipment growth in the United States remained slightly faster than most other regions in the third quarter and overall the U.S. PC market came in right on forecast with 4.3% year-on-year growth. Solid back-to-school sales, a strong performance from key vendors, the continued acceptance of Chromebooks, some commercial uptick from Windows XP to Windows 7 migration, and the slowdown in tablet sales are among the factors that helped the PC market to continue on its positive growth rate trajectory,” says Rajani Singh, Senior Research Analyst, Personal Computing. “Moving forward, we expect a healthy holiday season, hence the U.S. PC market may maintain a positive growth rate. However, low demand for large commercial refreshes, combined with competition from 2-in-1 systems, may limit the growth potential.”

Regional Highlights

United States – With shipments totaling 17.3 million PCs in 3Q14, the U.S. market grew by 4.3% from the same quarter a year ago and 2.6% from the previous quarter. Growth centered in strong momentum from the portables category, which grew by more than 9% year over year. Desktop shipments were relatively sluggish this quarter and growth remained in negative territory.

Europe, Middle East, and Africa (EMEA) – The PC market in EMEA saw another positive quarter with preparations for holiday sales fueling growth in shipments. Windows 8.1 with Bing notebooks contributed to higher sell-in numbers on portable PCs, particularly in the consumer space. Although demand related to the end of Windows XP support started to disappear, commercial shipments remained stable. Markets in Western Europe continued to drive the overall growth in EMEA, while shipments in the CEMA region remained constrained by economic and political instability.

Japan – Volume was better than expected although growth remained deeply negative. As expected, the volume of commercial activity slowed considerably, as many Windows XP projects came to completion. None of the top vendors saw either year-on-year or sequential growth, with market leader Lenovo falling below 900,000 units for the first time since the fourth quarter of 2012.

Asia/Pacific (excluding Japan) – Though still seeing a decline compared to last year, the region outperformed expectations. Modest economic growth in developed markets like Australia, New Zealand, and Singapore helped PC purchases to remain healthy. Stronger consumer demand for back-to-school season also helped to offset the lack of large public deals shown in the previous quarter. A transitioning period in the political climate in Southeast Asia caused lower public spending as expected. In China, public sector projects executed as part of the five-year plan and the improving U.S. economy helped, and likely brought China’s total PC shipments up to slightly higher than forecast levels.

Vendor Highlights

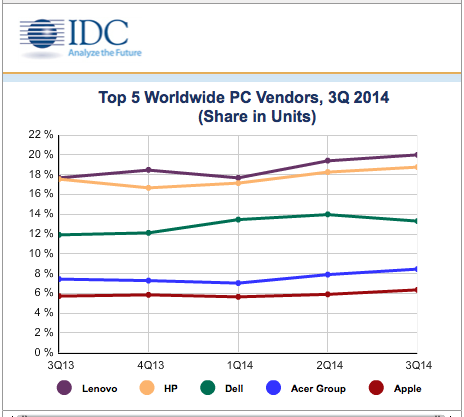

Lenovo held a comfortable lead as the top PC supplier, hitting another record volume of 15.7 million units. The vendor managed to regain growth in Asia/Pacific (excluding Japan) as well as maintain its strong pace of expansion and growth in EMEA.

HP shipped 14.7 million units and remained in the number 2 position with growth surpassing 5%. EMEA and mature markets continued to be the vendor’s primary sources of growth, as were some last-minute public sector notebook shipments.

Dell shipped over 10 million units, growing 9.7% on the year, much of it based on a strong performance in notebooks in the U.S. and Asia/Pacific (excluding Japan)

Acer grew over 11%, in part due to low volume a year ago but also from the success of its Chromebooks and entry-level notebooks

Apple moved into the number 5 position on a worldwide basis, slightly overtaking ASUS. The company’s steady growth, along with recent price cuts and improved demand in mature markets, has helped it to consistently outgrow the market.

Source: IDC Worldwide Quarterly PC Tracker, October 8, 2014

Table notes below.

Table Notes:

– Some IDC estimates prior to financial earnings reports.

– Shipments include shipments to distribution channels or end users. OEM sales are counted under the vendor/brand under which they are sold.

– PCs include Desktops, Portables, Ultraslim Notebooks, Chromebooks, and Workstations and do not include handhelds, x86 Servers and Tablets (i.e. iPad, or Tablets with detachable keyboards running either Windows or Android). Data for all vendors are reported for calendar periods.

– IDC’s Worldwide Quarterly PC Tracker gathers PC market data in over 80 countries by vendor, form factor, brand, processor brand and speed, sales channel and user segment. The research includes historical and forecast trend analysis as well as price band and installed base data.

IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC’s Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly excel deliverables and on-line query tools. The IDC Tracker Charts app allows users to view data charts from the most recent IDC Tracker products on their iPhone and iPad.

For more information, visit:

http://www.idc.com