Smartphone Momentum Still Evident with Shipments Expected to Reach 1.2 Billion in 2014 and Growing 23.1% Over 2013 – IDC

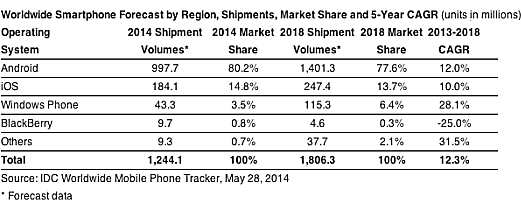

According to a new IDC Worldwide Quarterly Mobile Phone Tracker forecast, worldwide smartphone shipments will reach a total of 1.2 billion units worldwide in 2014, marking a 23.1% increase over 2013. From there, total volumes will reach 1.8 billion units in 2018, resulting in a 12.3% compound annual growth rate (CAGR) from 2013–2018.

“What makes smartphone growth so amazing is where the growth will be taking place,” said Ramon Llamas, Research Manager with IDC’s Mobile Phone team. “Smartphone shipments will more than double between now and 2018 within key emerging markets, including India, Indonesia, and Russia. In addition, China will account for nearly a third of all smartphone shipments in 2018. These – and other markets – will offer multiple opportunities to vendors and carriers alike, but the key will be balancing affordability with expectations.”

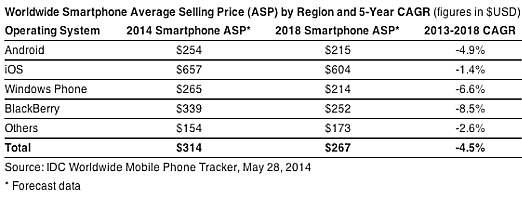

On a worldwide basis, IDC expects the average selling price (ASP) of smartphones to reach $314 in 2014, down 6.3% from the $335 ASP in 2013. From there, ASPs are expected to reach $267 by 2018. While these prices point to a definite decline, users still expect top-notch experiences regardless of what smartphone they purchase.

“Until recently, low cost has equaled poor quality in the smartphone space,” said Ryan Reith, Program Director with IDC’s Worldwide Quarterly Mobile Phone Tracker. “Given the competition at the high end, vendors like Motorola are trying to skate to where the puck is going by offering extremely affordable devices like the Moto E, which offer a ‘good enough’ experience that will suit the needs of many. This goes to show that components that were used 2-3 years back in high-end smartphones are still sufficient in many aspects, and ultimately will allow vendors to come to the table with viable low-cost solutions.”

Operating Systems

Android –Android will undoubtedly remain the clear market leader among smartphone operating systems with share expected to hit 80.2% in 2014. Looking forward, IDC expects Android to lose a minimal amount of share over the forecast period, mainly as a result of Windows Phone growth. Android has been, and will continue to be, the platform driving low-cost devices. ASPs of Android smartphones were well below market average in the first quarter of 2014 and are expected to be $254 for full year 2014, dropping to $215 in 2018. Growth of Android phones is expected to outpace the market in 2014, rising 25.6% with volume just shy of 1 billion units.

iOS – Despite rumors of a larger screen iPhone, IDC expects share of iOS to drop from 14.8% in 2014, to 13.7% in 2018. Apple continues to be strong in mature markets, where devices are heavily subsidized, but emerging markets are expected to drive overall market growth, and appetite for smartphones in these markets is at the sub-$200 level, significantly below Apple’s selling prices. iOS volumes are expected to hit 184.1 million in 2014, growing to 247.4 million in 2018. Growth of 20.0% this year will slowly drop to year-over-year growth of 6.1% in 2018, more in line with overall market growth.

Windows Phone – Windows Phone continues to slowly build its global footprint, and growth is expected to outpace the market throughout the forecast period. In 2014, volumes are expected to grow 29.5% over 2013, reaching 43.3 million shipments. This momentum is expected to continue into 2015, reaching 65.9 million units, continuing on to 115.3 million in 2018. It is somewhat unclear what Microsoft has in store for its recent acquisition of Nokia, but an additional positive is the number of new OEM partners recently announced. At Microsoft’s Build conference this year, the company announced a number of key features that had been visibly absent from the platform in the past. If more OEMs get behind the platform, and device portfolios continue to scale the cost spectrum, Windows Phone can continue to gain momentum.

BlackBerry OS – IDC continues to reduce its BlackBerry forecast across the board with volumes expected to drop 49.6% in 2014, equivalent to 9.7 million units. Looking forward, volumes are expected to continue to decline to 4.6 million units in 2018. The question of whether BlackBerry can survive continues to surface, and with expectations that share will fall below 1% in 2014, the only way the company will be viable is likely through a niche approach based on its security assets.

In addition to the table above, an interactive graphic showing worldwide smartphone share by geographic region over the 2012-2018 forecast period is available here. The chart is intended for public use in online news articles and social media. Instructions on how to embed this graphic can be found by viewing this press release on IDC.com.

For more information, visit:

http://www.idc.com